the convex answer to a complex question

As equity investor concerns increase over lower beta return expectations from the market portfolio, increased levels of correlations between fixed income and equities and ever higher levels of benchmark concentration, the focus shifts to portfolio construction. By extending our existing Smart Alpha framework we have developed a set of positively convex, all equity portfolios that simultaneously magnify upside returns and hedge downside risks – providing a best-of-all-worlds solution to equity risk and return.

Convexity is a bond concept that, in simple terms captures the non-linear nature of the relationship between an asset price and another factor. In bonds this is most obviously seen with interest rates. Bond prices rise when interest rates fall (and vice versa) – but not in a completely linear fashion. A bond with positive convexity is one where it gains more (in price) when interest rates fall than it loses when interest rates rise by the same amount.

Such positive convexity is clearly desirable and, when the concept is extended to equities, is a clear way to compare portfolio level returns to a benchmark such that positive convexity reflects out-performance relative to the benchmark – where gains exceed losses and especially so at both extremes, when market moves shift dramatically.

The “payoff curve” from such a strategy bends upward and, when constructed using options (this is typically how such convex strategies are constructed using OTM calls or options overlays) is considered Gamma positive. Performance during periods of low volatility can be subject to a cost drag, but ultimately, they are designed to provide a magnification of upside returns whilst hedging downside risks – a best of all worlds type scenario.

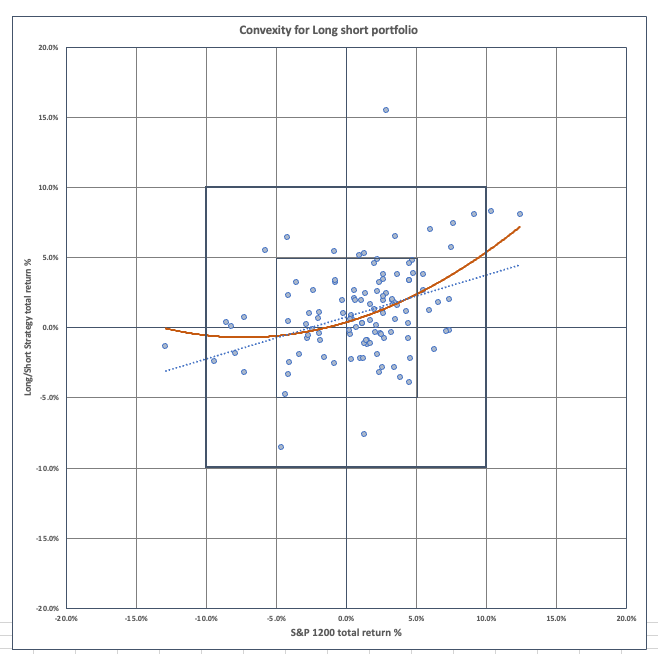

Creating a genuinely convex portfolio is not an easy task and if it involves the use of expensive put and call options may not provide a sufficiently attractive tool for risk management to be worth pursuing – especially in periods of relative market calm. However, we believe it is possible to devise such a portfolio using a sophisticated, Complex Adaptive System (CAS) based systematic investment approach that can provide something far closer to an “all weather portfolio” for equities through portfolio construction. Freed from a long-only approach or the need for expensive option overlays, a long-short strategy that has a low correlation to the underlying investment universe but has a clear, convex payoff curve is clearly possible and the Apollo Smart Alpha solution that we have developer is shown in the accompanying chart.

Equities are always about risk

Publicly listed equities are meant to be the “risky asset” in an investor portfolio. As an asset class, the risk that equities pose is that they may not provide the period return expected of them; undermining the ability for an investor to match, with sufficient certainty, the period-return on assets with an investor’s existing period-liabilities. Traditional portfolio construction methods follow two approaches to deal with this problem. Firstly, a widely diversified portfolio of equities is held, mitigating stock specific risk, and effectively creating “the market portfolio” of investment theory. Secondly, to balance the uncertainty of equity returns, the (near) certainty of bond returns are added to the mix, with the added benefit of reinforcing risk (volatility) management given the traditionally non-correlated nature of returns at the asset class level. The classic 60:40 portfolio is often the result: typically yielding an annualised 7% rolling 10-year return within a relatively tight range.

Is risk actually being managed?

The problem with this approach is that, with bonds delivering an annualised 2.5% return over the period – and with significant Sovereign Debt drawdowns over the last decade – the bulk of that return still comes from equity but at a 50% discount to a 100% Equity portfolio (the 10-Year annualised total return from the S&P1500 (US large, medium, and small caps) for example is 14%). And whilst the rolling 10-year annualised return of the 60/40 portfolio might be relatively stable, the periodic swings associated with it are not. Problems for this approach were compounded in 2022 when the typical 60/40 fund dropped by around 16% and bonds failed to act as any form of hedge against equity losses – raising the question as to what role this form of portfolio model is designed to play as far as risk management of the risky assets is concerned. With bonds, once again “failing” the correlation test versus equities the multi-asset model is back in the spotlight for all the wrong reasons and begs the question as to whether a convex equity portfolio is the better solution?

Unlike the theory of portfolio diversification across asset classes being designed to mitigate equity risk, the realitywould appear to be that effective risk management in moments of equity stress is rarely the outcome. In fact, a 180-degree argument could be made: that the higher expected returns provided by equities are necessary to boost the overall investor return on low yielding bond assets to help match real investor liabilities. Far from bonds being a risk diversifier, equities are a return enhancer – but with a clear opportunity cost. The challenge has been compounded by the fact that, over the last three years, the S&P has been compounding at a 19% annualised rate – nearly three times the annualised rate for 60:40 (for reference the Smart Alpha Long Only Global portfolio has compounded at 24% over the last three years). So, in the absence of a clear risk offset role from bonds, the attraction of owning 100% – as opposed to 60% – equities is becoming hard to argue against – provided that the equity portfolio itself can be constructed in such a way as to be able to hedge its own downside risk.

Convexity to the rescue

The provocative question as to what role bonds should actually play in the investor portfolio is a topic for another day, but the reframing of equity risk and risk management promotes an interesting shift in the passive/active equity investment debate. If we accept that equities are a risky asset class but that they nevertheless are an essential part of an asset-liability matching solution so long as their risk is managed, then the role of equity returns management is central. The concept that passive equities can represent the market portfolio as an asset class in such circumstances is not an unreasonable one – but only if the risk of the market portfolio itself can be managed as part of the portfolio process and the negative-tail hedged effectively.

Given the performance cost and higher than anticipated (positive) correlation of passive equities with the 60/40 model, it is not clear that bonds are up to the task of providing diversification, but an active, low/non-correlating equity portfolio could be introduced that not only allows for the annualised returns from the low-cost tracker to be fully retained for asset/liability management purposes but could provide both a risk offset via non correlation and a means of actively augmenting the passive returns. If the structure of that low/non correlating portfolio was also convex in nature, then risk management would be actively enhanced at the total portfolio level.

This in turn raises the question as to whether the separation of investor portfolios into the real-world investor requirements of risk free, relative risk free, and risky buckets described by John Cochrane (amongst others) is possible – and indeed preferable – to achieve under this approach. So long as the asset and liability portfolio components (the relative risk-free bucket) are constructed appropriately, then a risky portfolio consisting of a collection of either long only or convex long/short equity strategies designed to be low/non correlating with each other, would appear to be the obvious route to take. (In fact, any assets can be in either the relative risk free or the risky bucket. The point here is that short of a requirement to ensure that the liability portfolio is matched by the relatively risk-free bucket, all other equity products can be placed inside a risky – but risk manageable – bucket.)

Equities as return generators

Rather than being concerned over lower beta return expectations from the market portfolio or over increased levels of correlations between fixed income and equities or ever higher levels of benchmark concentration, the focus can shift towards active risk-taking in the risky bucket, with the ambition of generating compound excess returns over and above the liability portfolio. If the equity component of the relative risk-free bucket is doing its job, then the so-called “long only constraint” – whereby negative views on stocks can only be expressed via relative underweight positions in a tracker type equity product – can be lifted under this framework and equities can take on the role of generators of excess return (over liabilities) within the risky portfolio.

To a degree this is already happening. The use of “extension strategies” (also referred to as long/short beta-1 strategies) where both long and short side views are expressed with respect to an underlying index or universe along with “Portable Alpha” strategies where market exposure is gained via derivative exposure and then matched with uncorrelated sources of alpha (typically via Hedge Fund strategies) are becoming more widespread. These fit nicely into the risky bucket -along with variations of market neutral long/short equity strategies where downside tail risk is actively managed within the strategy itself. We believe that we can productively add to this collection of products using a convex strategy model derived from the Smart Alpha framework.

Smart alpha evolution – management of risk AND return

Motivated by this shift towards a more active and less constrained environment, the ability to introduce more hedge-fund like exposures to those using existing long only portfolios would appear to be a natural evolution of the Apollo Smart Alpha process. Utilising the long and short stock selection and risk management capabilities of the Apollo framework, a research project was undertaken to examine firstly how effective and integrable a long/short stock selection process might be using Smart Alpha before constructing a series of systematic, back-tested, extension/enhanced and long/short portfolio strategies for global equity markets.

What started out as a research project has led to just such an evolution of Smart Alpha. Not only does the analysis confirm the validity of the Smart Alpha process beyond the “long only constraint” – its ability to consistently identify and exploit short side returns in a systematic and consistent way is on a par with the long side results – it is also able to deliver a fully integrable stock selection solution for both the extension and market neutral portfolios. The low benchmark/strategy correlation and convex nature of the returns (see chart) suggests a genuine “all weather” portfolio product can be systematically generated that has the added benefit of being completely integrable across a range of similar Smart Alpha portfolios that can be tailored to almost any required asset/liability requirements.

In the research report (now published), we conclude that such diversified equity products are not only viable investment strategies, but a potentially invaluable set of risk managed extension and leveraged equity portfolio component products. The robust, integrated nature of both the risk management and return generation processes are confirmed, and this reinforces the role that a systematic, active approach to equities can provide outside of the traditional passive or quasi-active tracker roles that equities have migrated to over the last two decades. Either individually or as part of an integrated investment solution, these allow for compound excess returns to be built up over time, shifting the focus towards multi-period investment under a dynamic, equity-based, risk and return framework.

If you are interested in seeing a copy of the report, please comment below.